Resources

Blogs

Popular Routes

Transfer Hotspot

Trusted Providers

Comparison

About

FAQs

Resources

Blogs

Popular Routes

Transfer Hotspot

Trusted Providers

Comparison

About

FAQs

Sign In

Upgrowth

Get the App, Skip the Hassle

Download our app and carry the experience wherever you go.

Frequently Asked Questions

Suggested Articles

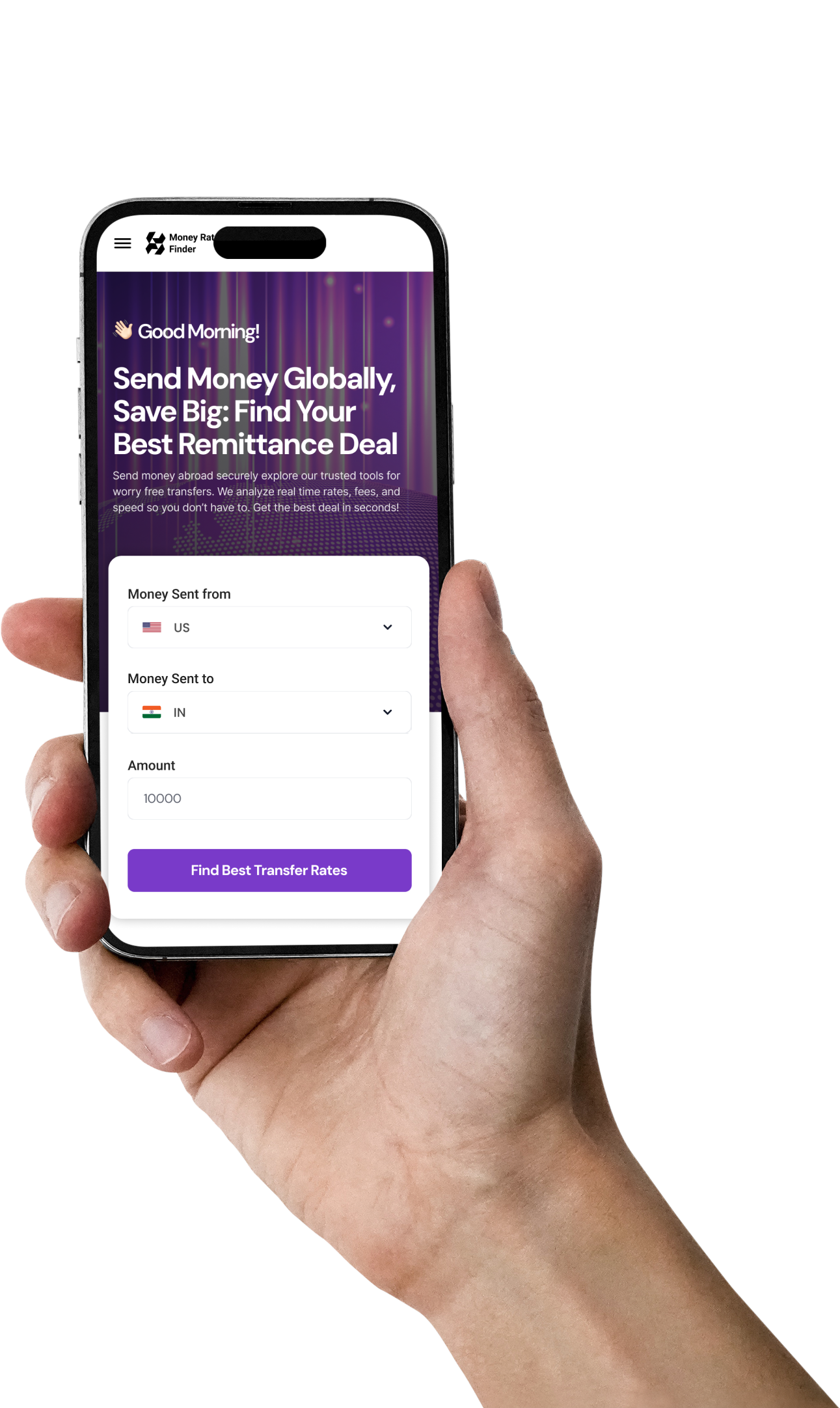

You send

They receive

Amount

Find Rates